.svg)

Support at Home contributions explained

See what you'll pay under Support at Home: 0% for clinical care, means-tested rates for other services, a lifetime cap, and no-worse-off protection.

Author: Sensible Care

Support at Home contributions are the out-of-pocket amounts you pay for non-clinical supports, while clinical care is 0% when it's on your plan. Your share is a percentage of the service price, set by a means test and limited by a lifetime cap. If you're moving from a Home Care Package, no-worse-off protections apply.

Under Support at Home, you will contribute toward some day-to-day, non-clinical supports, and the government will cover the rest.

Your out-of-pocket costs are called Support at Home contributions.

Clinically required care (nursing or physiotherapy on your approved plan) is fully funded, so you don't have to pay anything for those services.

In this article, we'll talk about how contributions work for the three Support at Home service types.

You'll also learn about typical ranges, the lifetime cap rule, and "no-worse-off" protections for current Home Care Package recipients.

If you need help at any point, Sensible Care can walk you through your assessment, statements, and service options.

What are Support at Home participant contributions?

Support at Home contributions are the out-of-pocket expenses you pay for certain non-clinical home supports.

The Australian Government pays the rest of the bill as a subsidy.

With the shift from Home Care Packages to the Support at Home program, clinical care will become fully subsidised. If a clinical service (like nursing or physiotherapy) is on your approved care plan, your contribution is 0%.

Contributions apply to everyday support services, which may include:

- Personal care (e.g., showering, dressing)

- Domestic help (e.g., cleaning, laundry)

- Meal preparation and shopping

- Some consumables

- Assistive technology

- Minor home modifications

Your contribution is a percentage of the service price. You only pay for what you receive - no charges for unused services or standby time.

How to calculate your contribution?

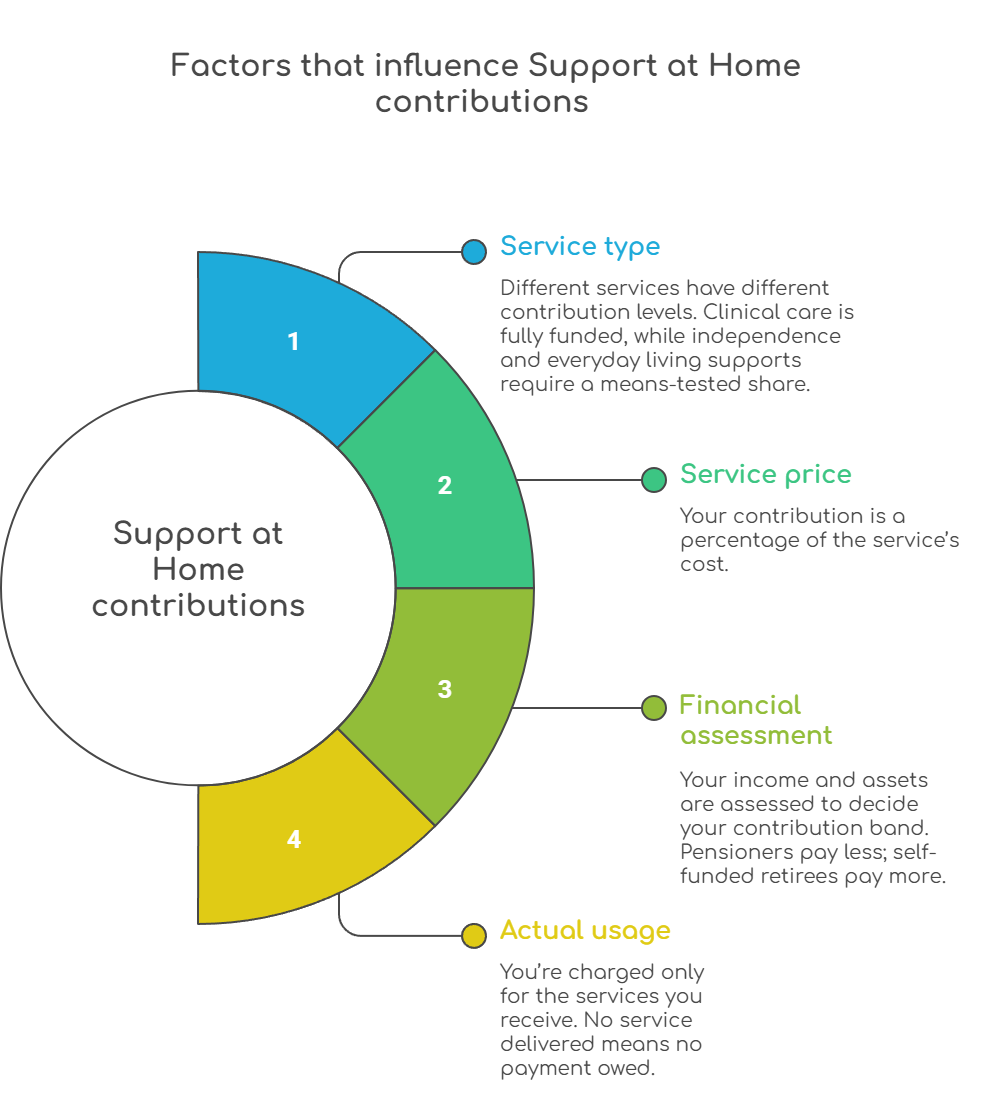

Your out-of-pocket amount isn't a flat fee. It's worked out each time you receive a service. Four factors affect what you pay:

- Service type

- Service price

- Your financial assessment

- How much you actually use

Service type

Support at Home distinguishes three service types. Each type has different funding rules and contribution levels.

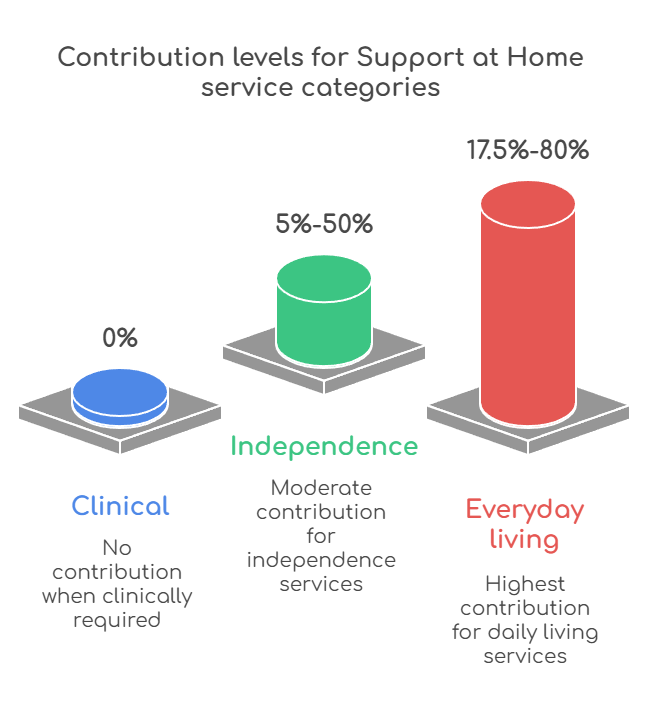

- Clinical (e.g., nursing, physio): 0% contribution when clinically required and on your plan.

- Independence (e.g., personal care, assistive technology, minor home modifications): moderate contribution.

- Everyday living (e.g., domestic help, meal preparation, shopping): highest contribution.

The same person could pay 0% for a nurse visit and 17.5% to 80% for domestic help, because they're different service types.

Clinical services (0% contribution)

These are medical or therapeutic supports provided by qualified health professionals. It could include nursing, wound care, or physiotherapy.

When the service is clinically required and listed in your approved care plan, you pay nothing. The Australian Government covers the full cost of delivery.

Independence services (moderate contribution)

This category covers supports designed to help you maintain or improve your independence at home and stay safe.

Examples include:

- Personal care (showering and dressing)

- Installing assistive technology

- Minor home modifications

Contributions for these services are means-tested, ranging from 5% for full pensioners to 50% for self-funded retirees.

Everyday living services (higher contribution)

These are day-to-day tasks that keep your home running smoothly, like:

- Cleaning

- Laundry

- Meal preparation

- Gardening

Because they're not clinical or directly tied to medical need, they have the highest contribution rates.

Depending on your financial situation, you may contribute between 17.5% and 80% of the service cost.

Service price

Each service has a price.

In the first year of the Support at Home program, providers will set their own prices within government guidelines. This allows for flexibility while the system transitions from Home Care Packages.

From 1 July 2026, official price caps will come into effect to ensure fairness and consistency across all providers.

Your contribution is a percentage of that price.

Even if your contribution percentage stays the same, your dollar amount will change depending on the price of each service.

For example, if a cleaning service costs $100 and your contribution rate is 17.5%, you'll pay $17.50. If the same service costs $120, your contribution increases to $21, because your share is based on the higher price.

With older programs, providers could add separate charges. Support at Home requires transparent pricing. This means:

- Service prices must reflect the entire cost of delivering that service (e.g., worker time, administration/overheads, travel/transport).

- Care management is funded separately: 10% of your quarterly budget is automatically set aside in a pooled care management account for planning and coordination, and appears as its own clearly itemised line (not bundled into each service price).

- No separate "package management" fees and no hidden add-ons outside the published service price and the itemised care management allocation.

Your financial assessment

Your Support at Home contributions may also depend on your financial assessment.

This process ensures contributions are fair and based on your capacity to pay, rather than a one-size-fits-all fee.

The review considers your personal income, or your joint income if you're a couple, and your financial resources. The assessment excludes your home and car, but it factors in savings, investments, and other income sources.

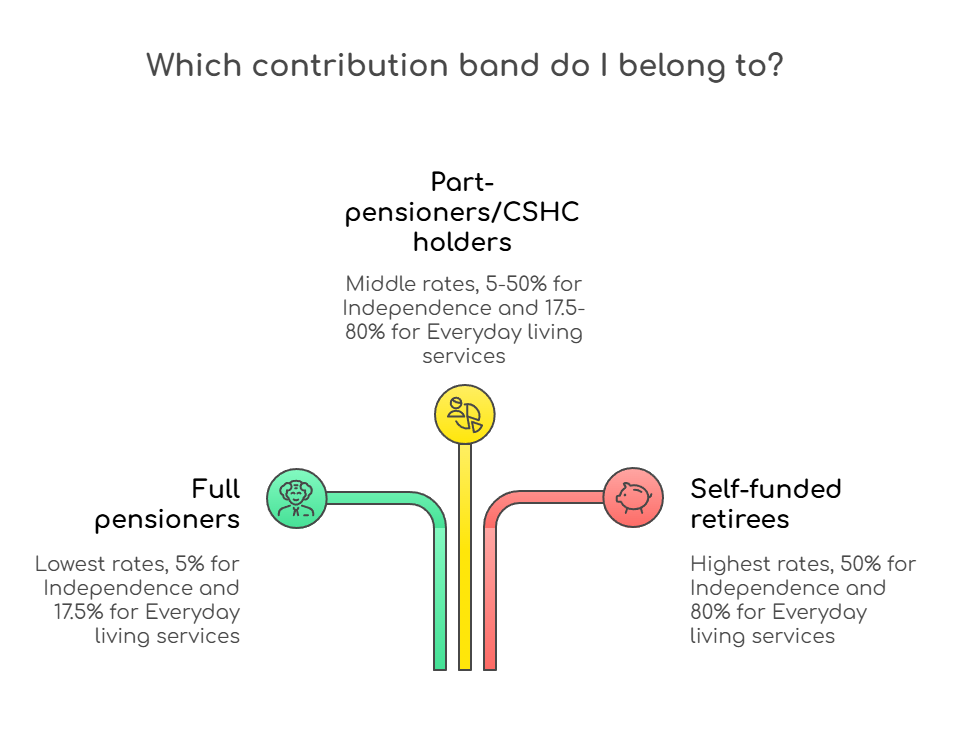

Once your assessment is complete, you're placed into a contribution band:

- Full pensioners pay the lowest contribution rates, often just 5% for Independence services and 17.5% for Everyday living supports.

- Part-pensioners and Commonwealth Seniors Health Card (CSHC) holders (including self-funded retirees who hold a CSHC) fall into middle bands, with means-tested rates between 5% and 50% for Independence and 17.5% to 80% for Everyday living.

- Self-funded retirees without concession cards contribute at the highest rates, typically 50% for Independence and 80% for Everyday living services.

Your financial assessment ensures the system remains fair and transparent. Those with lower incomes receive more government support, while those with greater means contribute more.

It also means your contribution is tailored to your circumstances, helping keep essential care affordable and accessible.

How much you actually use

Support at Home operates on a pay-as-you-go basis, which means you're only billed for services you actually receive.

There are no standing charges or "retainer" fees. You only pay when a service is delivered. Late cancellations/no-shows may still attract a charge.

Each time you receive a service, whether it's an hour of personal care or a domestic help visit, it's logged by your provider. The cost of that service is then split between you and the government according to your contribution rate.

If you need to cancel, give at least two business days' notice. Cancellations with sufficient notice aren't charged. If you cancel late (under two business days) or miss an appointment, the provider may be paid in full, and you may be charged your normal contribution for that service.

Your monthly/quarterly statements will show:

- The service type (Clinical, Independence, or Everyday living)

- The full-service price

- Your contribution (both the percentage and dollar amount)

- The government subsidy that covers the rest

This transparency helps you see exactly what you're paying for and ensures your total spending stays within your budget.

Quick "how it works" examples

- Everyday living (domestic help): Price $100, your rate 17.5% → You pay $17.50, Government pays $82.50.

- Independence (personal care): Price $110, your rate 10% → You pay $11, the government pays $129.

- Clinical (nurse visit): Price $120, your rate 0% → You pay $0, the government pays $120.

Contributions for existing Home Care recipients

The "no-worse-off" rule applies if you were:

- Already receiving a Home Care Package (HCP)

- Approved or on the waiting list on or before 12 September 2024

This protection ensures that moving to the new program won't increase your costs.

Your out-of-pocket contributions won't increase because of the program change. You'll pay the same or less than you did under HCP for comparable non-clinical support.

It also means you'll have a discounted contribution schedule (a lower lifetime cap of $84,571.66). This uses lower percentages than the standard Support at Home rates for new entrants.

If your needs change later and you're reassessed, the no-worse-off settings still prevent you from paying more because of the reform.

How to confirm you're covered:

- Check your My Aged Care letters or portal for your transition status.

- Ask your provider to confirm which contribution schedule they're applying to you.

- If something looks off on your invoice, raise it with your provider first; they can check with My Aged Care/Services Australia.

How the lifetime payment cap works

Support at Home has a built-in safeguard called the lifetime cap. It limits how much you can pay for non-clinical services over your lifetime.

Once your total contributions reach the cap, you stop paying for these types of support. The Australian Government covers the full cost from that point on.

The lifetime cap is $135,318.69 (as of 20 September 2025). This amount is indexed twice a year (on 20 March and 20 September) to keep up with inflation and cost changes.

The lifetime cap only applies to non-clinical services. Clinical care (like nursing or physiotherapy) is fully funded and never counted toward the cap.

Services Australia tracks your payments automatically, so you don't need to do anything to monitor your progress.

If you were already receiving a Home Care Package, you may have a lower lifetime cap under the no-worse-off protection rules.

This system ensures that your total out-of-pocket costs for non-clinical support stay fair, predictable, and within a clear limit.

How contributions link to residential aged care

If you transition from Support at Home to residential aged care in the future, your contributions follow you.

The lifetime cap applies across both settings - home care and residential care.

For residential aged care, there are two ways the cap can be reached:

- Dollar limit: When your total non-clinical care contributions reach $135,318.69 (indexed), or

- Time limit: After you've been paying contributions for four years, whichever comes first.

Any contributions you make under Support at Home will count toward both these limits.

Let's say you've already paid $50,000 in Support at Home contributions. You would then only need to pay $85,318.69 more (or less, depending on indexing) in residential care before reaching the dollar cap.

This combined approach ensures you're protected from excessive lifetime costs. The same applies when you receive care at home, in residential aged care, or both.

FAQ

Do I have to pay for clinical services like nursing or physiotherapy?

No. If a clinical service is approved as part of your care plan, it's fully funded by the government. You won't pay a participant contribution for it.

Which services do I contribute to?

You'll usually contribute to non-clinical supports such as personal care, domestic help, meal preparation, etc. These fall under Independence or Everyday living services.

Do I pay for cancelled or unused services?

No, you're charged only for the services you actually receive. If a service is cancelled ahead of time with adequate notice (typically 1 business day), there's no charge for that day.

When do government price caps start?

Providers set their own prices until 1 July 2026. After that, government price caps will apply to ensure prices stay consistent and reasonable.

Making Support at Home simple, fair, and affordable with Sensible Care

The Support at Home program makes it easier to see what you pay, what's covered, and how much protection you have.

With clear contribution rates, automatic lifetime caps, and built-in safeguards for existing Home Care clients, the system aims to keep home supports affordable and transparent.

At Sensible Care, we know these changes can be confusing — but you don't have to figure them out alone. Our friendly team can help you:

- Understand your Services Australia assessment and contribution rate.

- Review your care plan and statements for accuracy.

- Arrange the right mix of services to suit your needs and budget.

Contact Sensible Care today or book a free consultation to discuss your Support at Home plan. We'll ensure you understand your options and get the care you deserve without paying more than you should.

Take the Next Step in Care

Download our Info Kit or speak to one of our friendly team members today.

Explore More Helpful Reads

More stories, guides, and updates to support you and your family.

Need Help Getting Started?

Reach out on your terms, pick a time that suits you and let’s talk about how we can help.

.webp)